Understand your small business plan financials

Breaking down key financial statements

Do you drive a car? Most of us do. Do you turn on the ignition, put the car in gear, and then close your eyes when you’re driving? That would be inviting catastrophe.

If you don’t know how to read the financial statements of your business, you’re driving your business with your eyes closed. It’s not a surprise, so many small businesses fail; it’s miraculous even a few survive, since most business owners cannot understand what their top three financial statements are telling them.

Think of your numbers like your spouse. They’re always talking to you, but you’ve got to learn to listen to what they’re saying. If you do, you’ll make better business decisions and avoid becoming a statistic like most of your peers.

"Your numbers, or your financial statements, are the global positioning system for your business."

If you read this full article, you will know more about basic financials than 90% of small business owners out there. Don’t just skim this article, read it for understanding to the very end. I think you’ll find it an important and worthwhile investment.

Your numbers, or your financial statements, are the global positioning system for your business. These reveal the true financial health of your business. Most entrepreneurs are optimists by nature, so we always think our businesses are in stronger financial shape than they actually are.

Let’s keep things simple. As a business owner, you must be able to answer three key questions at all times.

- Are you making money? Look at your net income statement.

- Do you have enough cash to pay the bills next month? Look at your cash flow statement.

- Are you building owner’s equity or destroying it? Look at your balance sheet.

Types of financial statements

There are really only three primary financial statements that will answer these three questions. The hosts on Shark Tank never tell you that!

- Net income statement measures profitability.

- Cash flow statement measures how much cash is required to run the business and for how long.

- Balance sheet measures the state of owner’s equity since the business started.

You can easily understand each one. Turn off your cell phone, close your Facebook feed, and focus with me. Here we go…

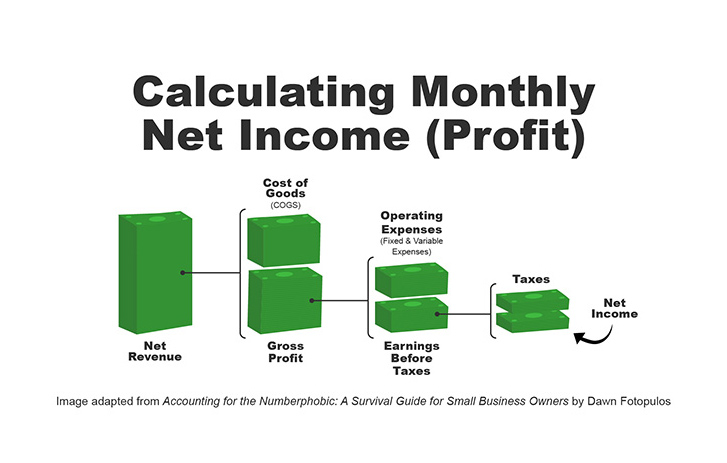

The net income statement — are you making money?

Making money refers to profitability. Profitability is the same thing as your bottom line. It’s what’s left over from sales after you’ve accounted for all the expenses of your business. This includes paying your suppliers, your employees, accountant, lawyer, operating expenses, and taxes. If your business is profitable, you have money left over. This is what you want.

Think of your net income statement like a pile of money that gets smaller as you pay your expenses. You start with net revenue, which for this illustration is your sales less discounts or returns. COGS is shorthand for cost of goods sold or your direct expenses.

If you sell T-shirts, this would include direct labor and direct materials like the cost of the fabric, screen printing, and sewing. This is what is required to produce a finished product for sale. If you deduct COGS from net revenue, you’re left with something very important: gross profit. You run the rest of the business and pay all your operating expenses from gross profit.

Fixed expenses are things like rent. Variable expenses are things like marketing expenses. When you deduct fixed and variable expenses (or operating expenses if taken together) you’re left with earnings before taxes, and then of course, you have to pay taxes.

"That’s hard to achieve, but keeping expenses as low as possible for as long as possible will help get you there."

The money that’s left after taxes are paid is what you get to keep. That’s net income. That number is why you’re in business. The larger the bottom line or net income number is, the more viable your business is. According to Greg Crabtree, CPA, for every dollar in revenues your business generates, fifteen cents needs to drop to the bottom line.

That’s hard to achieve, but keeping expenses as low as possible for as long as possible will help get you there. Look at your net income statement at the end of each month.

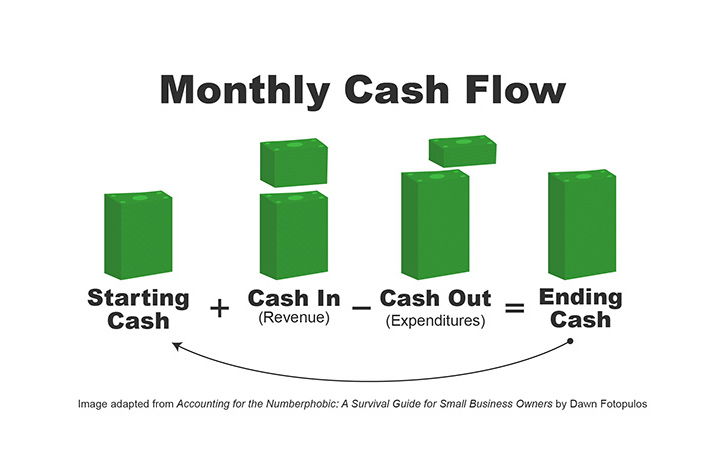

Cash flow statement — enough cash to pay the bills?

Cash is to your business as blood is to your body. If you run out of blood, you die. If you run out of cash, your business dies. The reason why just measuring profitability is not enough is because not all profit converts into cash flow.

Sometimes there are time lags; you do the job, the client pays you weeks later. Sometimes the client never pays their bill, and you have to write off those revenues. Until revenues or sales convert into cash flow, you’re not out of the woods.

Did you know that your business could be showing a profit and still be going bankrupt? It’s true. That’s why measuring how much cash you have, how much you need, and how much you anticipate coming into the business is so important.

Imagine a bucket with a spigot. The water in the bucket is your cash flow. When a client pays their bill, that increases the water level. That’s great! As you pay your bills, the spigot opens and cash flows out of the business.

At the end of the month, you are left with an ending cash position. This is your starting cash position for next month. You’ll use this cash plus any new revenue from sales to pay next month’s bills. You don’t have to create this financial report; your bookkeeper or CPA can do this for you. Plan to look at this report at the end of each week.

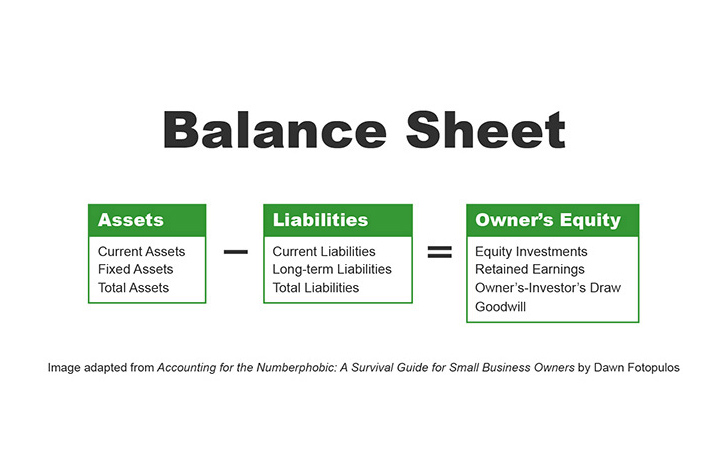

The balance sheet — are you building owner’s equity?

After you’ve tracked profit and cash flow, the balance sheet captures the ebb and flow of the business since the first day you started. This is the statement every banker or investor will look at first. It seems a little complicated, but if you break it down, you realize there are only three parts to a balance sheet.

It doesn’t matter if you’re running Facebook or the corner deli, the balance sheet structure is always the same. In the first section you have assets. These are all the things you own. The categories you’ll see captured in your asset base include cash assets or assets that can convert into cash.

The second section is called liabilities. This is what you owe to others and could include short-term debt (like credit cards and supplier credit) or long-term debt (like a mortgage), as well as any associated interest payments.

If you take what you own (assets) and deduct what you owe (liabilities) the difference is owner’s equity. What you’re after is an asset base that’s larger than your liabilities. That means you have a positive owner’s equity or net worth. This is what you want.

Look at your balance sheet every month or at least every quarter. If your interest charges are starting to climb, speak to your CPA, bookkeeper, or banker to find ways to lower them. They can get out of hand quickly.

If you’re doing a great job of marketing and customers love your products, then your business will be generating lots of gross profit, which will help your asset base grow faster than your liabilities. This is what you want over the long term.

Congratulations! You now know more than most of your peers. The concepts in this article were taken from the book, Accounting for the Numberphobic: A Survival Guide for Small Business Owners published by AMACOM Books. Check it out if you’d like to learn how to improve gross margin, net income, and owner’s equity. And always feel free to reach out to let me know how you’re doing!

Looking for more? Find more of my small business financial resources at the FedEx Small Business Money Management page and at DawnFotopulos.com.

Dawn Fotopulos is associate professor of business at King’s College. A “recovering banker” with more than 20 years of experience in the banking industry, Dawn is an expert in entrepreneurship and has guided hundreds of struggling small businesses to recovery. She is also the award-winning author of Accounting for the Numberphobic: A Survival Guide for Small Business Owners.

Related reading

9 ways to stay on budget with smart shipping

Get simple tips for getting the most value and savings with FedEx. These include signing up for discounts and rewards, and more.

read article

Exploring angel investing

Owner, Gina Cucina, details why she decided to seek angel investing for her small, growing business.

read article

Crowd-funding for small business

Small business owners Kelly McCollum and Marcie Colledge from Yellow Scope share the secrets of successful crowdfunding.

read articleNote: The information provided in this website does not constitute legal, tax, finance, accounting or trade advice, but is designed to provide general information relating to business and commerce. The FedEx® Small Business Center’s content, information and services are not a substitute for obtaining the advice of a competent professional, for example a licensed attorney, law firm, accountant or financial adviser.